The First Crypto Purchase of 2027 Won't Happen on an Exchange

Tiger Research and SVB predict fintech apps will overtake exchanges as the primary crypto entry point in 2026. Robinhood, Revolut, and PayPal are already there. Here's what it means for your keyword strategy.

It will happen inside a banking app. The user won’t know they’re touching a blockchain. They’ll tap “invest,” pick Bitcoin, and go back to checking their balance. No seed phrases. No exchange signup. No new app.

This isn’t a prediction. It’s already happening.

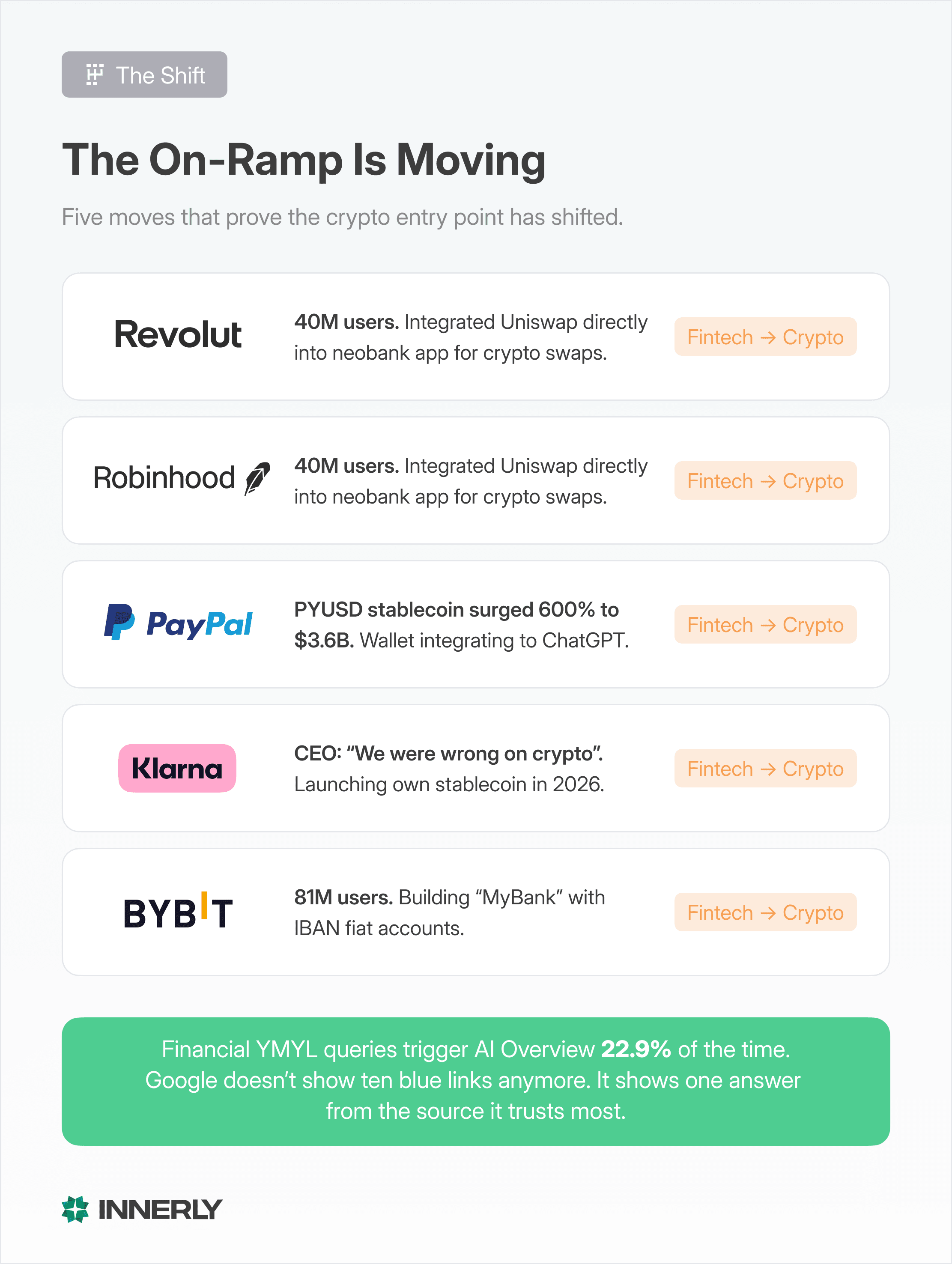

Revolut just integrated Uniswap directly into its neobank app, giving 40 million users access to decentralized exchange swaps alongside their salary deposits. Robinhood processed $4.6 trillion in trading volume last year, launched tokenized shares across Europe, and is now positioning itself as a financial “super-app” that happens to include crypto. PayPal’s own stablecoin PYUSD surged 600% to $3.6 billion in circulation. Klarna, the buy now pay later giant that rejected crypto in 2022, announced plans to launch its own stablecoin in 2026. Its CEO’s public reversal: “We were wrong on crypto.”

Tiger Research and CoinGecko called it in their 2026 market outlook: fintech platforms, not exchanges, will become the primary on-ramp to crypto.

The data backs it up. SVB’s 2026 crypto predictions put it plainly: the breakout consumer apps won’t market themselves as “crypto.” They’ll feel like modern fintech with stablecoin settlement running quietly under the hood.

For growth teams at crypto companies, this is the most important competitive shift of the year. And most are still marketing like it’s not happening.

The On-Ramp Is Moving

The reason fintech apps are winning the on-ramp isn’t technology. It’s trust and simplicity.

A new user who wants to buy their first Bitcoin faces two options. Option one: download Coinbase or Binance, complete KYC, fund an account, navigate a trading interface, and learn enough crypto vocabulary to feel confident clicking “buy.” Option two: open the Revolut app they already use for groceries, tap “crypto,” and buy Bitcoin with the money already in their account. Same outcome. One takes twenty minutes and a learning curve. The other takes thirty seconds and zero new context.

Tiger Research identified this as a structural shift, not a temporary trend. As regulatory clarity improves globally, fintech apps gain the legal certainty to integrate crypto buying, selling, and holding directly into their existing interfaces. The GENIUS Act in the U.S. and MiCA in Europe have given these platforms the frameworks they needed to move aggressively.

Robinhood’s crypto head Johann Kerbrat set the tone for 2026: “creating a faster, smarter, and more connected future for each investor.” Revolut’s crypto head of product Leonid Bashlykov was even more direct: “2026 is going to be massive.”

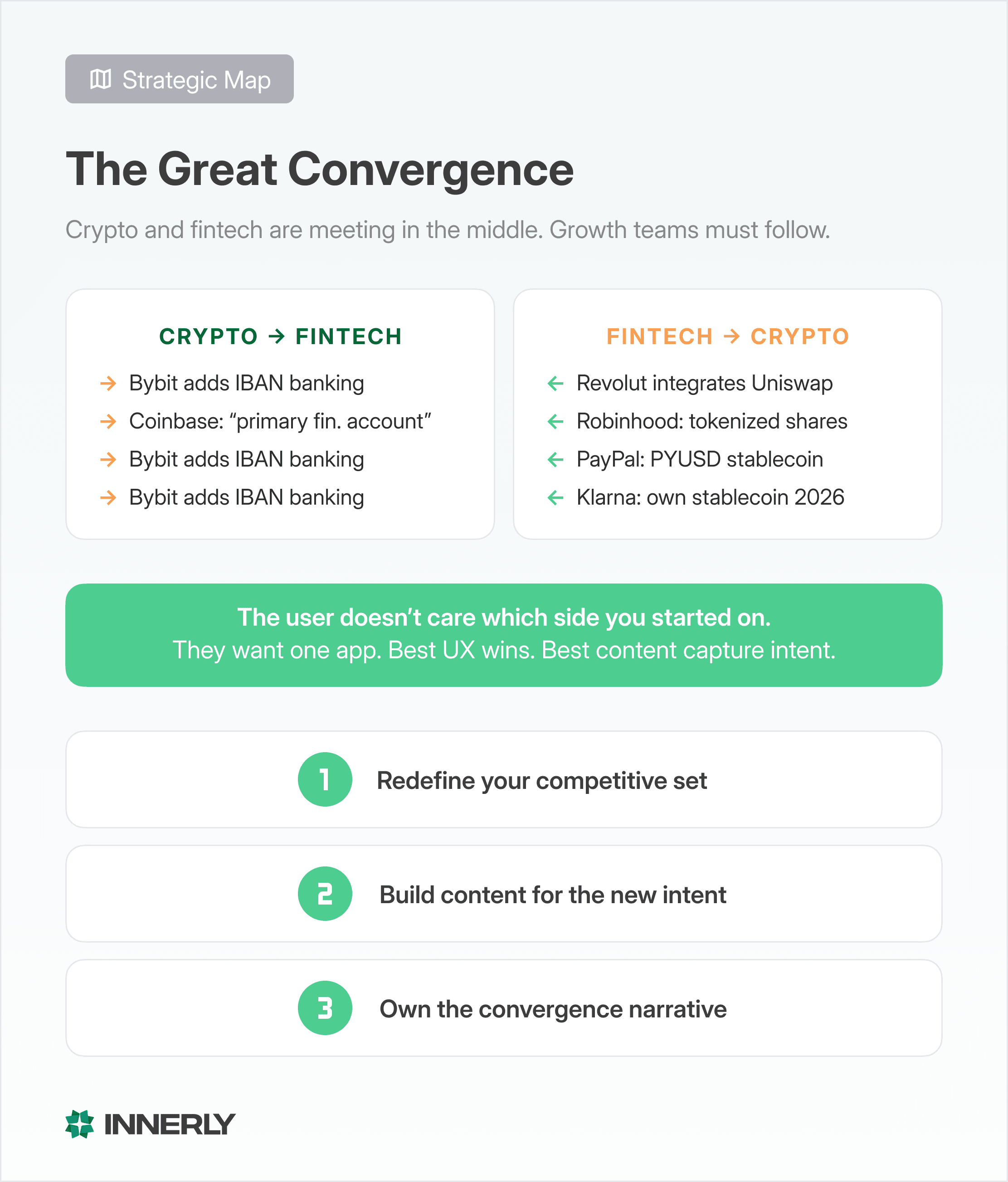

Meanwhile, the traffic flows in one direction. Bybit, one of the largest crypto exchanges, is building “MyBank,” a product that lets users hold fiat currencies with IBANs. The exchange is becoming a neobank. Coinbase CEO Brian Armstrong stated the company’s ambition plainly: “We want to become people’s primary financial account.”

Exchanges are trying to become fintech apps. Fintech apps have already become exchanges. The question is who gets there first with the better user experience.

Why Growth Teams Should Care

Here’s where this shifts from a product story to a marketing story.

When the primary crypto on-ramp was an exchange, the keyword landscape centered on crypto native intent. “Best crypto exchange.” “How to buy Bitcoin on Coinbase.” “Binance vs Kraken.” Growth teams optimized for these queries, built comparison content, and ran paid campaigns targeting crypto curious audiences.

That keyword landscape is eroding.

The new queries look different. “Best app to invest money.” “Revolut vs Robinhood for beginners.” “How to invest small amounts.” These are fintech queries, not crypto queries. The user doesn’t think of themselves as entering the crypto market. They think of themselves as using a financial app that happens to include crypto as one feature among many.

For crypto exchanges, this means your competitors aren’t just other exchanges anymore. They’re Revolut. They’re Robinhood. They’re Cash App. They’re every neobank that added a “crypto” tab to an app with millions of existing users.

For fintech companies, this means the organic search opportunity is massive and largely uncontested. Most neobanks are building the crypto product but not building the content strategy around it. The search demand exists. The content doesn’t. That gap is where growth teams win.

Three Things to Do Now

-

Redefine your competitive set. If you’re an exchange, start tracking fintech app keywords alongside exchange comparison keywords. If you’re a fintech, audit whether your crypto features are even visible in organic search. Most neobanks bury crypto functionality deep in their apps and create zero discoverable content around it.

-

Build content for the new intent. The user searching “best way to invest $100” doesn’t know they’re a potential crypto customer. Content that bridges financial planning intent with crypto exposure, written with E-E-A-T compliance and structured data, captures demand before it ever reaches an exchange.

-

Own the convergence narrative. The fintech and crypto audiences are merging. The companies that create authoritative content explaining this convergence, connecting it to regulation, user experience, and practical investment guidance, will build entity authority in both verticals simultaneously. That’s a compounding advantage.

The Clock Isn’t Ticking. It Already Rang.

Revolut: 40 million users. Robinhood: “super-app” positioning with crypto, stocks, retirement, and prediction markets in one interface. PayPal: PYUSD at $3.6 billion and growing. Klarna: from “we don’t do crypto” to launching a stablecoin in under three years.

Every one of these platforms already has the user base. They don’t need to acquire crypto customers. They just need to activate features for the customers they already have.

For exchanges, the defensive play is becoming a fintech app. For fintech companies, the offensive play is owning the keyword landscape before competitors realize it’s shifting. For both, the content strategy that wins in 2026 speaks to users who don’t identify as “crypto people” but will own digital assets within the year.

The on-ramp moved. The growth teams that follow it will find a bigger market on the other side.